Silicon Valley Bank and the Modern Bank Run

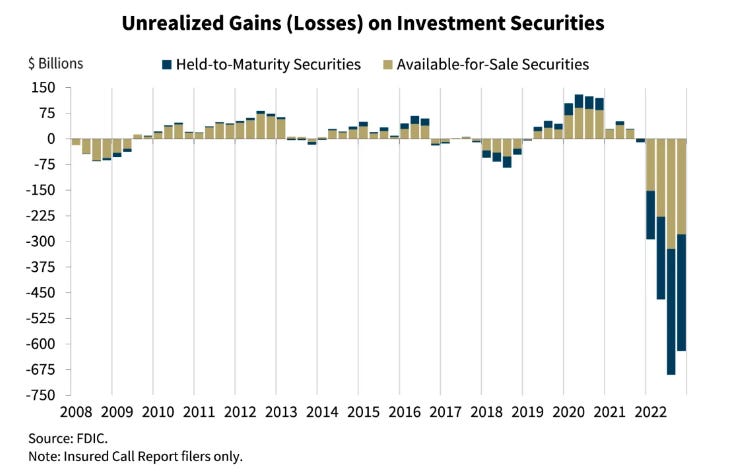

On Friday March 10, Silicon Valley Bank (SVB) was declared insolvent after $42 billion in deposits were withdrawn in a single day. SVB’s insolvency was due to their failure to hedge against interest rate risk. When the Fed rapidly raised interest rates in order to combat inflation, it not only affected people seeking loans, it also negatively impacted the balance sheets of banks holding long duration securities with fixed interest rates. When interest rates rose, the value of SVB’s fixed interest rate securities fell. The secondary market value of these securities doesn’t matter if a bank can meet its liabilities up until the securities mature, but then SVB was hit with a bank run.

A Modern Bank Run

SVB banked lots of the startups in Silicon Valley. By the end of 2022, SVB managed over 170 billion USD worth of deposits but only about 10% of it was insured. Once the big money in Silicon Valley smelled a weak balance sheet, people began withdrawing in mass while pleading for government intervention on social media. The bank run was on. At the end of the day, SVB didn’t have the cash to cover their liabilities, so they were taken over by the Federal Deposit Insurance Corporation (FDIC). The insolvency of SVB marked the third largest banking failure in US history.

The Central Bank and Government Intervenes

On Sunday March 12, the Federal Reserve, Treasury, and FDIC released a joint statement announcing they were making SVB depositors whole and that all depositors would have access to their money the next day. The Fed also announced a new lending facility created to help banks struggling to “meet the needs of all depositors”. The Treasury is also backstopping the Fed’s emergency lending facility up to $25 billion, meaning that if banks using the emergency facility default on the Fed, the Treasury covers the losses.

Moral Hazard or Elegant Intervention?

The bank run and government intervention will change the ways banks perceive risk. On one hand, this is a wake up call for banks that didn’t hedge against interest rate risk to make a more resilient balance sheet: banks will likely think about other ways they are at risk of insolvency due to volatile markets. On the other hand, banks are also aware that if they make a mistake, the Fed will step in as lender of last resort and the Treasury will pay up in case anything goes wrong.

The Fed also did something unusual in how money is traditionally loaned. Loans are usually extended with collateral valued at the market rate. Instead, the Fed is offering loans and valuing the collateral at “face value,” aka the amount paid back to the investor at maturity. Extending these loans may avert a crisis, but we will need to wait and see if this just kicked the problem further down the road.